April’s inflation rate of 7.2% is not just an unpleasant surprise; it is a reminder of how quickly macroeconomic stability can unravel when external shocks meet domestic vulnerabilities.

For households, it shows up immediately in higher food and fuel costs. For businesses, it appears in thinner margins, unpredictable input prices, and a more cautious consumer base.

After months of relative calm, the Philippine economy has been jolted back into a familiar bind—one where global energy markets, food supply fragilities, and currency weakness converge into a broad-based squeeze that neither consumers nor firms can easily absorb.

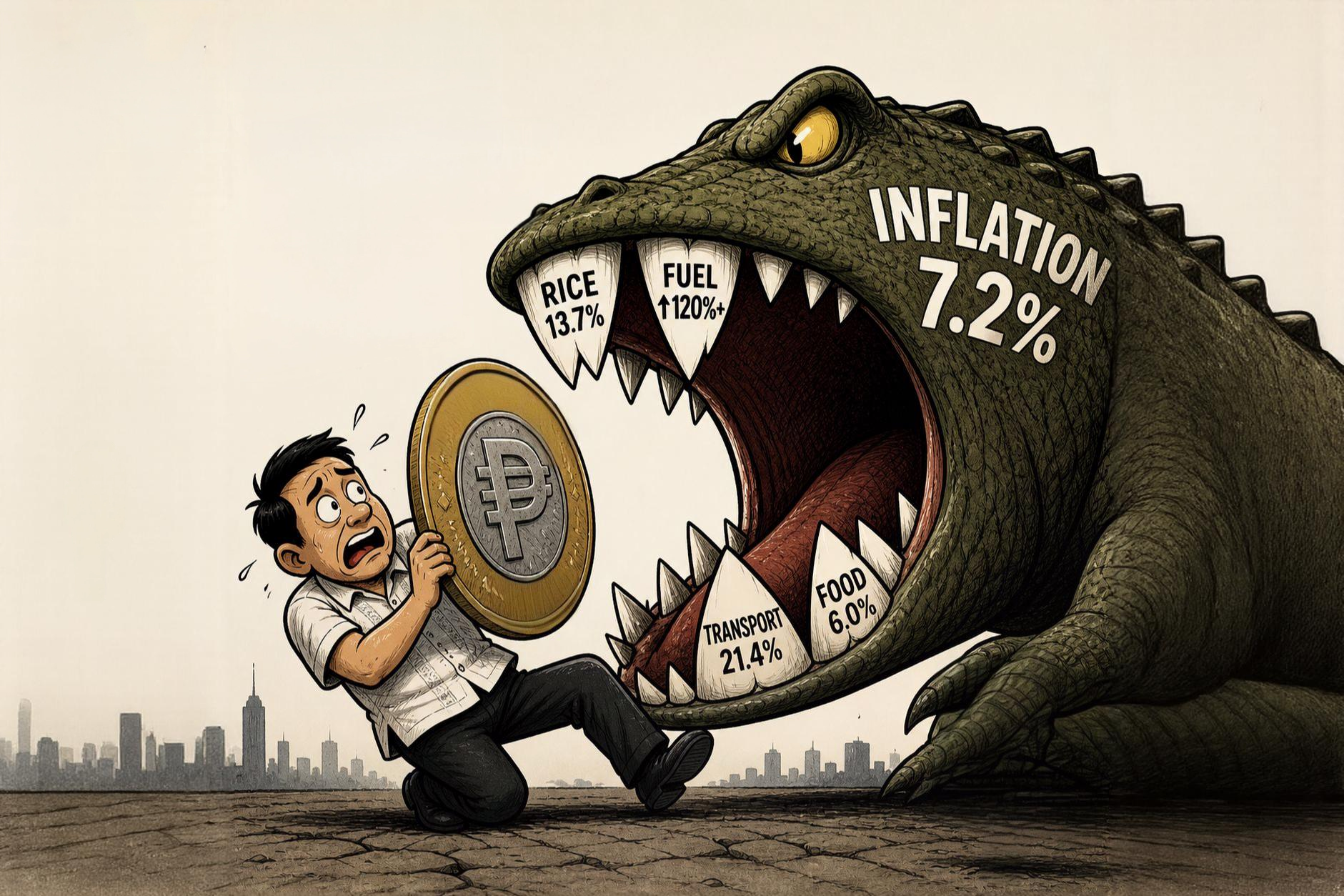

The headline figure from the Philippine Statistics Authority overshot nearly every benchmark that matters: the Bangko Sentral ng Pilipinas target range of 2% to 4%, market expectations, and concensus forecasts.

That alone would be concerning. More troubling is the composition. Inflation is no longer confined to a narrow set of volatile items; it is diffusing across essentials that define both household spending and business operations—from staple food to fuel-dependent logistics.

Food, which accounts for the largest share of household spending, contributed more than a third of the increase. Rice inflation accelerating to 13.7% is particularly consequential in a country where it remains both a staple and a pricing benchmark for wage earners.

For families, it erodes daily purchasing power. For food producers, retailers, and restaurants, it complicates pricing decisions and inventory planning. This is less about temporary price noise and more about structural exposure—import dependence, supply chain inefficiencies, and climate-sensitive production.

Energy, meanwhile, is acting as both trigger and amplifier. The surge in transport inflation—driven by a more than doubling of diesel prices and sharp increases in gasoline—illustrates how imported oil shocks cascade through the economy.

Businesses feel this first through higher distribution and operating costs. Consumers encounter it through fare hikes and more expensive goods. Once fuel costs spike, they seep into logistics, public transport fares, and eventually the price tags across supermarkets and service providers.

This is where the narrative becomes less about inflation as a statistic and more about inflation as lived reality—and operational reality. The purchasing power erosion—₱1 in 2018 now effectively worth around 73 centavos—captures a cumulative strain that headline averages often obscure.

For the bottom 30% of households, facing inflation of 8.5%, the squeeze is sharper still. For businesses, especially small and medium enterprises, the dilemma is equally stark: pass on higher costs and risk losing customers, or absorb them and compress already tight margins.

Either way, spending slows, and economic momentum softens.

The currency adds another layer. The peso’s slide to above ₱61 per dollar reflects both global dollar strength and persistent capital outflows.

For import-dependent firms, this raises the cost of raw materials, fuel, and equipment. For consumers, it reinforces price increases on imported goods. It also complicates the central bank’s policy calculus.

Tightening monetary policy to defend the peso risks suppressing domestic demand further. Holding back risks entrenching inflation expectations that affect both wage negotiations and business pricing strategies.

Markets, for their part, are already registering unease. The decline in the Philippine Stock Exchange index (PSEi) and the cautious movement of the peso suggest that investors are recalibrating expectations.

Inflation at this level narrows policy space and raises uncertainty around growth trajectories. Thin trading volumes further hint at a wait-and-see posture—not just among investors, but among businesses delaying expansion and households postponing discretionary spending.

Yet the situation is not entirely unanchored. Average inflation for the first four months of the year remains within target, and core inflation, while rising, is still below headline levels.

This suggests that second-round effects—such as sustained wage-price spirals—are not yet fully embedded. The government’s mitigating measures, including fuel subsidies and fare discounts, may cushion the immediate blow, but they are palliative rather than curative.

The deeper issue is that the Philippines continues to operate with limited insulation from external shocks. Energy dependence, agricultural constraints, infrastructure inefficiencies, and a structurally weaker currency form a mix that repeatedly exposes both households and businesses to volatility.

Each inflation spike is treated as episodic, yet the pattern is cyclical—and increasingly costly for all sectors.

For policymakers, the challenge is not simply to bring inflation back within target but to address the conditions that make such overshoots recurrent.

That means investing in energy diversification, strengthening food security, upgrading infrastructure efficiency, and maintaining credible monetary policy without over-reliance on blunt tightening tools.

For the public and the business community alike, the adjustment is immediate and intertwined.

A 7.2% inflation rate is not just a number to be managed; it is a signal that the margin for policy error is narrowing.

The issue is no longer whether inflation will ease—it likely will as base effects fade—but whether the same structural weaknesses will remain, primed to amplify the next shock across households and businesses alike. Without reform, each cycle will not just repeat—it will compound.

Stay updated—follow Philippines Today on Facebook and Instagram, and subscribe on YouTube for more stories.